Sustainable Governance

永續治理

CTCI Implements IFRS to Strengthen Operations and Enhance Sustainability Disclosure Quality

A New Era of Sustainability Information Disclosure

In recent years, sustainability issues have received widespread attention. However, as there are many standards today, to make it easy for stakeholders to understand and compare, and to grasp the impact of sustainability issues on the company, the ISSB (under the IFRS Foundation) released IFRS S1 "General Requirements for Disclosure of Sustainability-related Financial Information" and IFRS S2 "Climate-related Disclosures" in June 2023. The release of these two standards signifies that sustainability information is officially aligned with financial reporting, becoming a core key for measuring corporate value. S1:Positioned as a general disclosure framework, it aims to provide information useful for investment decisions. It requires companies to disclose the financial effects of sustainability-related risks and opportunities, ensuring the completeness and comparability of information through the "Governance, Strategy, Risk Management, and Metrics and Targets" framework. S2:A specific standard for climate issues, focusing on "physical risks" and "transition risks" brought by climate change. Companies must disclose greenhouse gas emissions and apply "climate scenario analysis" to assess the level of impact, using this to develop transition plans and response strategies.

Benefits of IFRS Adoption and Alignment with Taiwan's Implementation Schedule

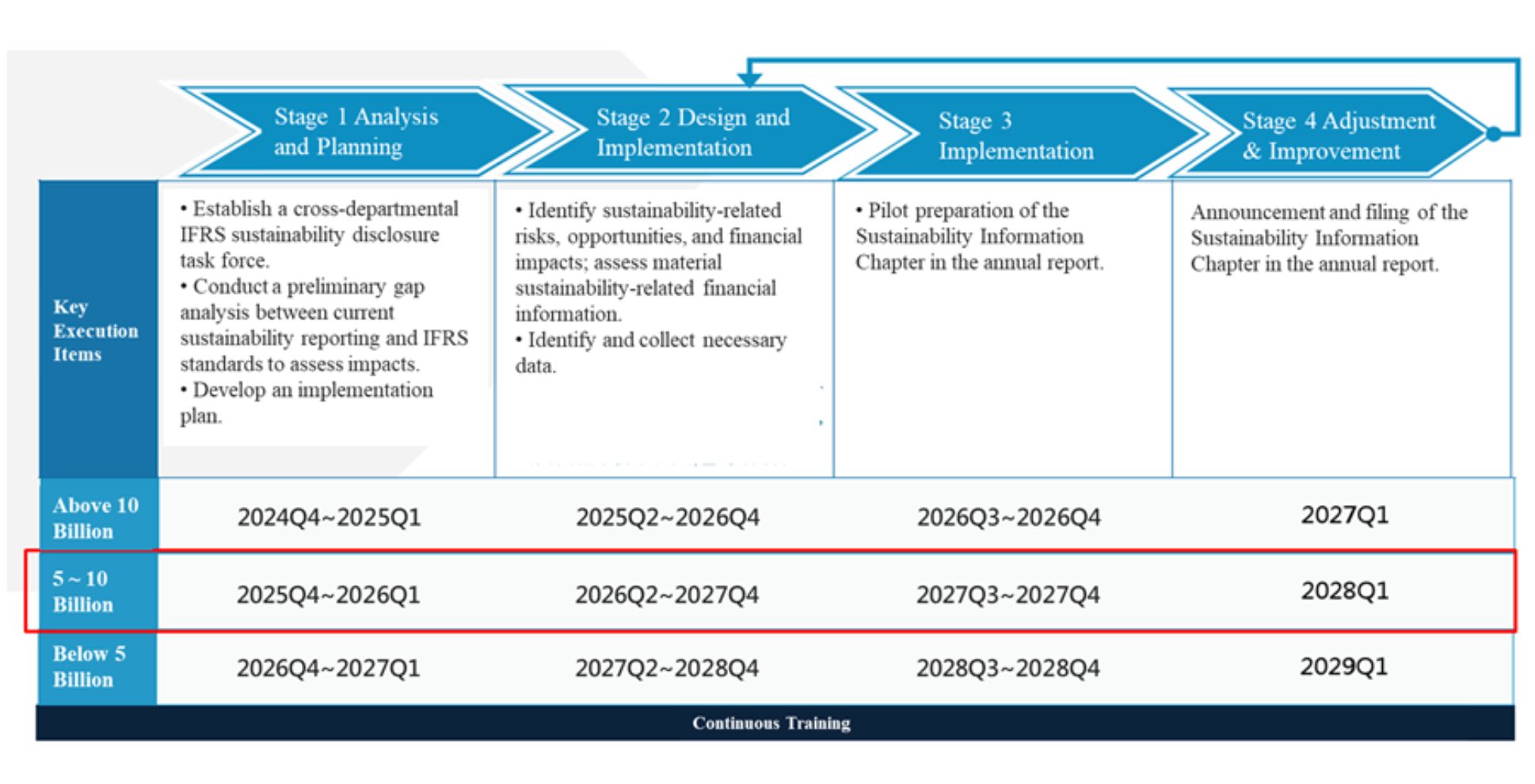

Adopting IFRS not only ensures compliance with international standards but also serves as a strategic opportunity to deepen corporate fundamentals and strengthen organizational resilience. Its benefits include: .Enhancing investor trust and reducing information asymmetry: IFRS provides a unified global language to eliminate "greenwashing" concerns. When companies disclose sustainability risks with financial-grade rigor, they can attract long-term value investors (such as sovereign wealth funds and labor pension funds). .Optimizing internal management and cross-departmental integration: Since sustainability issues involve multiple departments, it is necessary to establish cross-departmental information aggregation processes and internal control mechanisms to strengthen the accuracy and completeness of information. .Proactively addressing risks and seizing opportunities: Through the IFRS framework, companies can transform abstract risks into "quantified" financial impacts, moving from passive response to proactive risk mitigation. This also helps discover potential low-carbon green business or transition opportunities, improving market competitiveness while implementing carbon reduction. In response, Taiwan's Financial Supervisory Commission (FSC) released the "Roadmap for Taiwan's Alignment with IFRS Sustainability Disclosure Standards" in August 2023. Listed companies will apply the IFRS Sustainability Disclosure Standards in three batches based on their capital size. Each batch is planned in four stages, and the execution items for each stage must be completed within the timeframes specified by the FSC (as shown in the figure below). These must then be reported to the Board of Directors and filed with the Taiwan Stock Exchange (TWSE).

CTCI Implementation Schedule as a Second Batch Entity

CTCI belongs to the second batch and is expected to complete the dedicated sustainability disclosure chapter by 2028, to be included in the 2027 annual report. The governance body is using this as an opportunity to comprehensively review sustainability performance, drive gap improvements, optimize operations, and deepen the management of material sustainability issues. For Stage 1 (Analysis and Planning), CTCI’s progress is ahead of the FSC's required timeline, having been completed and approved by the Board of Directors by the end of 2025. Regarding Stage 2 (Design and Implementation), as of the end of February 2026, the identification of material sustainability issues has been completed, and relevant risks and opportunities have been clarified through impact pathway analysis, as explained below:

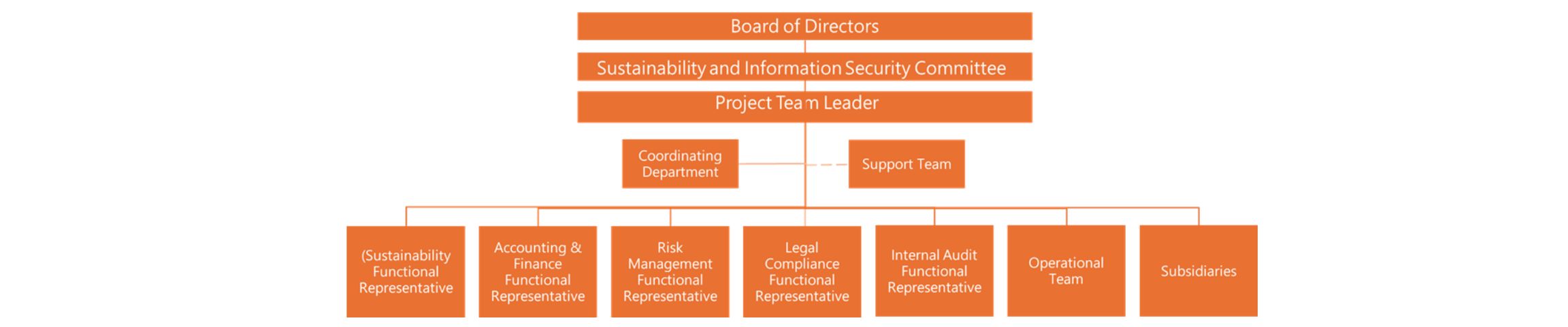

Establishment of CTCI IFRS Sustainability Disclosure Task Force

To ensure the smooth implementation of IFRS, CTCI established the IFRS Sustainability Disclosure Task Force in August 2025, with the Chief Sustainability Officer (CSO) serving as the leader. The task force fulfills the following roles: .Top-down Elevation of Governance Stature: Overseen by the Board of Directors and the "Sustainability and Information Security Committee," the task force is reported on by the CSO, demonstrating the importance management places on sustainability management. .Horizontal communication to strengthen issue promotion: Since sustainability issues are part of daily operations across various units—such as sustainability, finance and accounting, risk management, legal compliance, auditing, operations teams, and subsidiaries—the task force acts as an integrator, facilitating mutual understanding and exchange among units and linking them to financial aspects.

CTCI IFRS Sustainability Disclosure Task Force

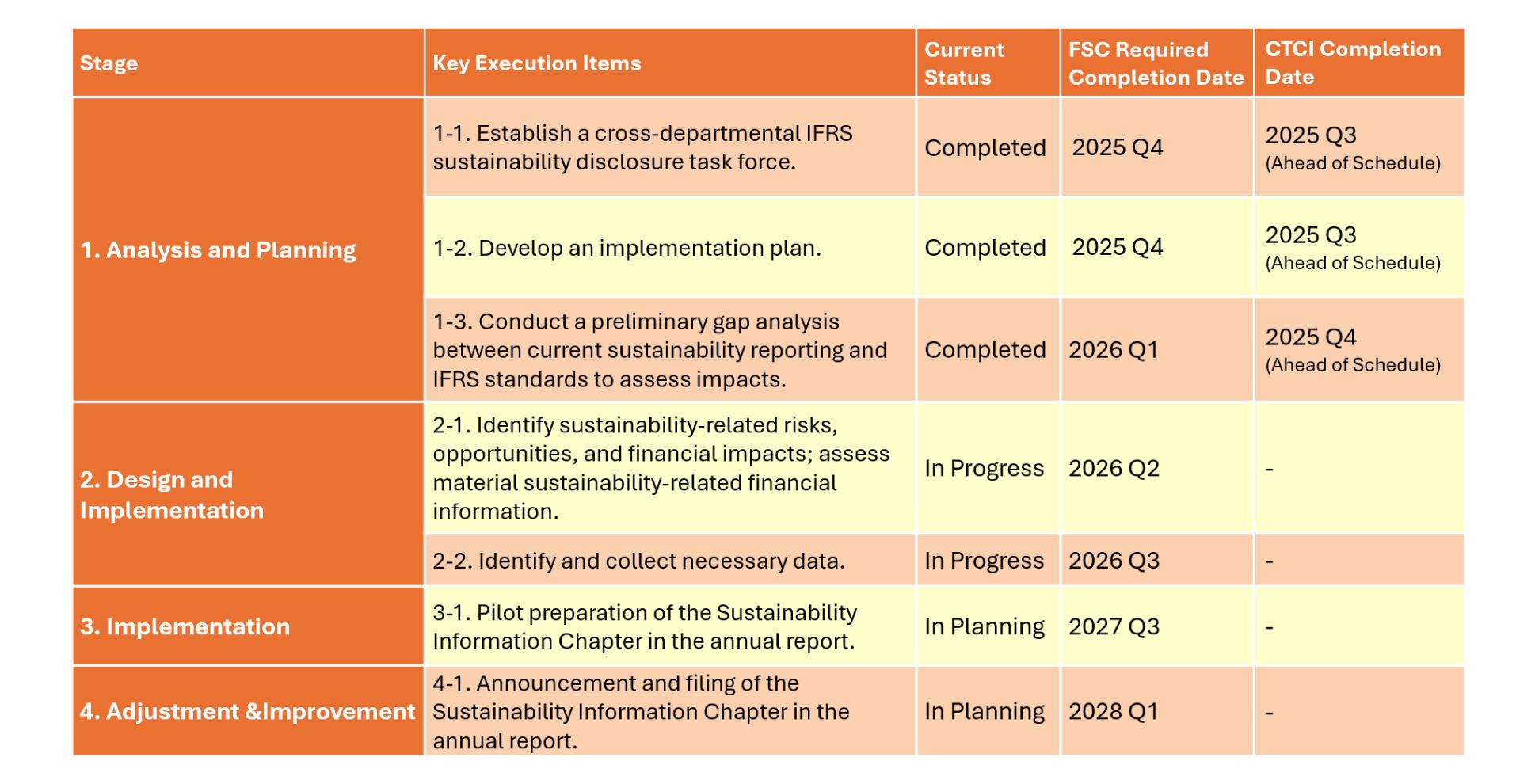

Establishing CTCI's IFRS Implementation Plan

To ensure the smooth completion of the sustainability chapter by 2028, CTCI has established an IFRS implementation plan, which plans execution priorities and implementation paths in stages to push various tasks forward. Stage 1 was completed ahead of the FSC's required timeline.

CTCI IFRS Implementation Plan

Conducting a gap analysis to identify four key areas for enhancement.

As IFRS S1 and S2 are new regulations, the Task Force reviewed existing public disclosure information, including sustainability reports, annual reports, and relevant websites, to understand CTCI's current level of compliance. Four directions for future improvement were identified: .Expansion of the Reporting Entity: The disclosure scope needs to expand from the current CTCI Corporation to include all subsidiaries within the consolidated financial statements. .Expanding from Climate to Sustainability: While previous focus was on climate-related financial risks and opportunities, it now needs to expand to "sustainability-related" risks and opportunities. .Quantifying Financial Impacts: Sustainability issues must consider their impact on the company's financial aspects, including current and expected financial performance, cash flow, assets and liabilities, and investment and divestment. .Enhancing Disclosure Transparency: Strengthening the explanation of parameters and assumptions in scenario analysis, the probability of occurrence, the level of impact, and uncertainty. Through the gap analysis, the Task Force has clarified the gap between CTCI and international disclosure standards. Follow-up actions will drive improvements and enhancements according to the implementation plan schedule. Regarding the execution process, material sustainability issues will first be identified, which will then be used to identify related risks and opportunities. Quantitative assessments will then be conducted through methods such as scenario analysis to further link them to financial impacts.

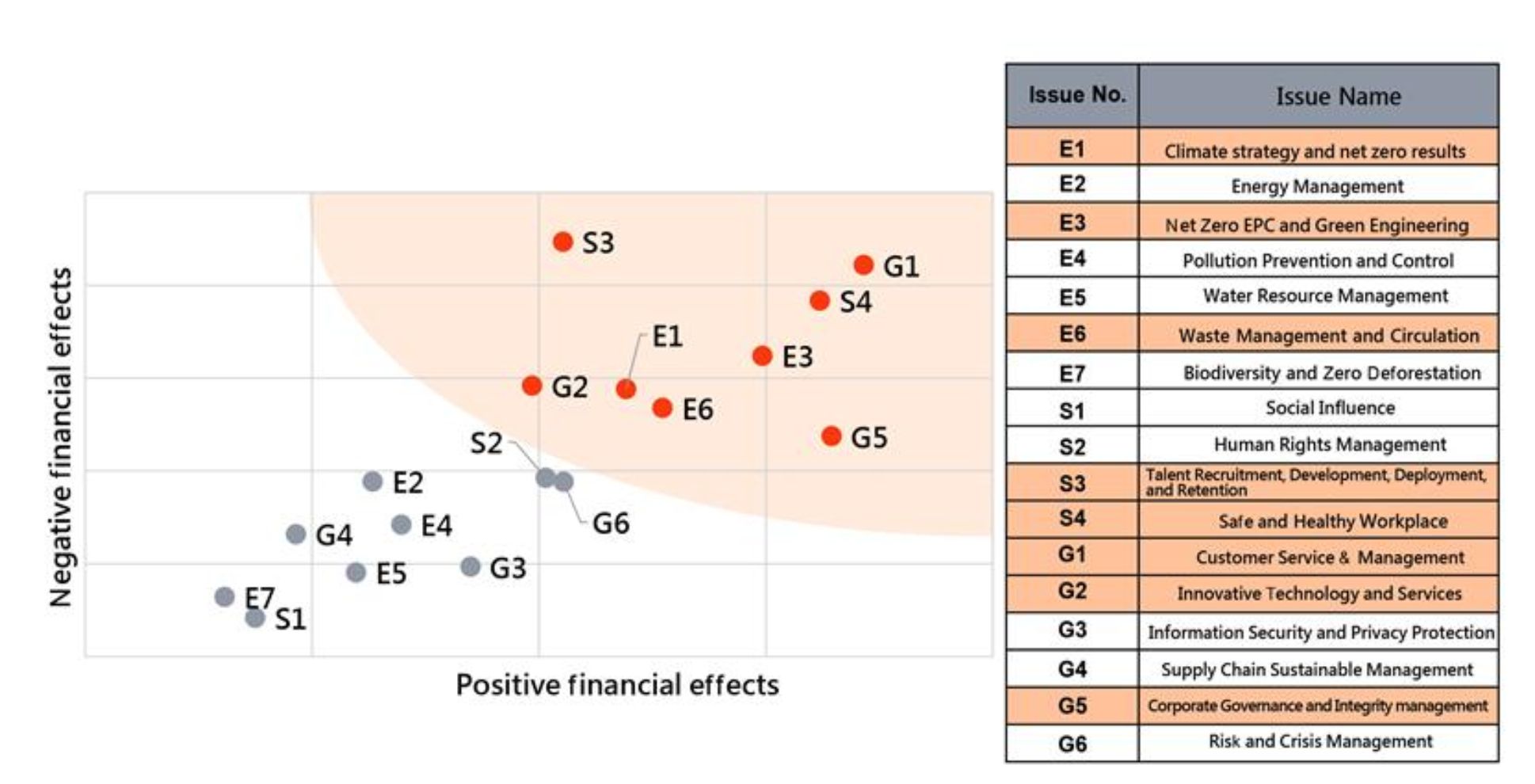

Identifying Material Sustainability Issues

The Task Force referred to the Sustainability Accounting Standards Board (SASB) industry standards. It selected "Engineering & Construction Services," "Waste Management," and "Software & IT Services" as the primary industry categories, summarizing 17 sustainability issues. Then, through a survey conducted by the Task Force, 8 material sustainability issues were identified via a matrix (3 Environmental, 2 Governance, and 3 Social).

Identifying Material Sustainability Issues via Matrix Analysis

Impact Pathway Analysis: Identifying Risks and Opportunities

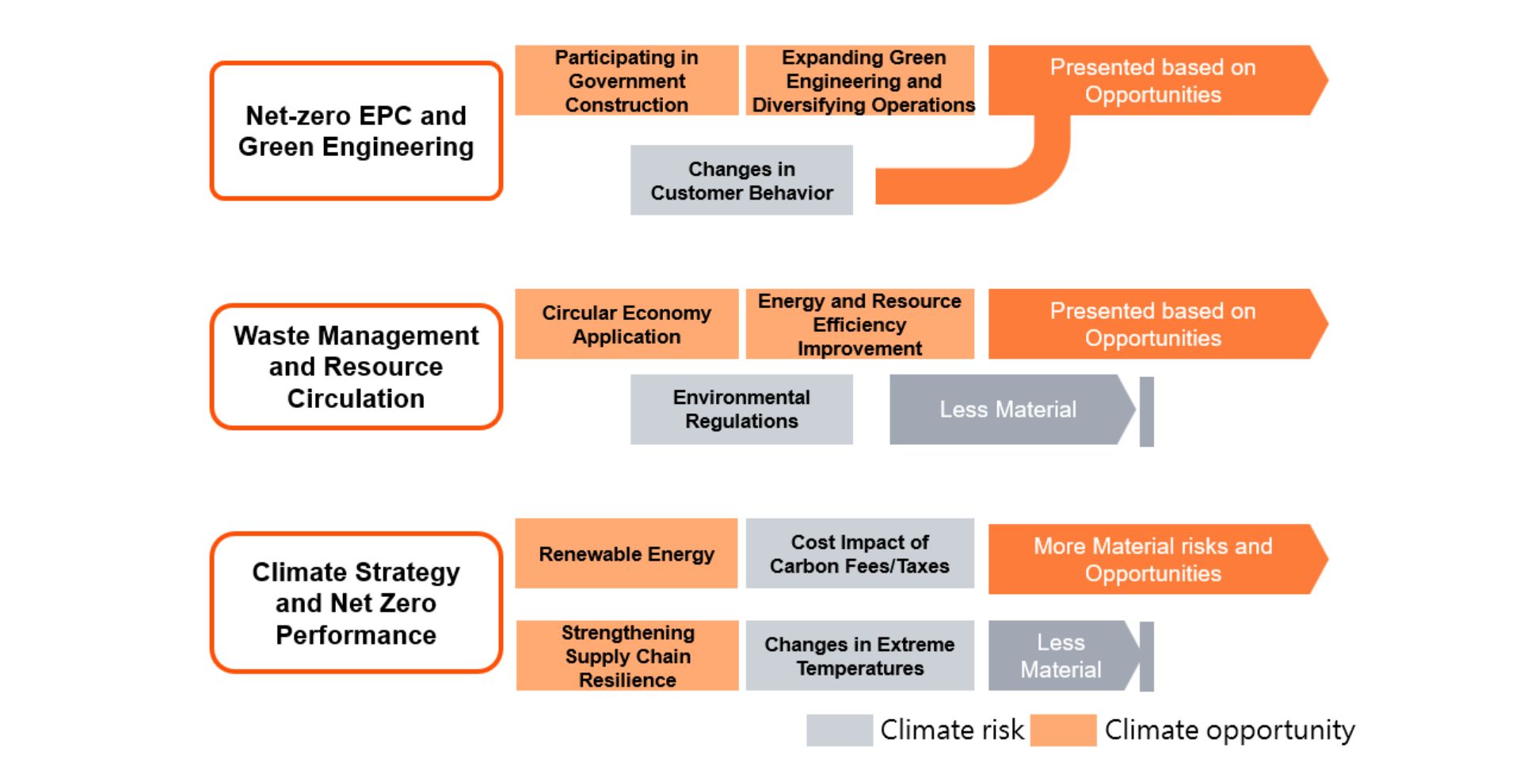

For the 8 material sustainability issues, the Task Force identified potential risks and opportunities through senior executive interviews. Taking "Net-zero EPC and Green Engineering" as an example, with "expanding green engineering and diversifying operations" as the primary development opportunity, CTCI has accumulated project track records in reclaimed water plants, rail engineering, Mr. Energy promotion, and Carbon Capture and Storage (CCS). Future directions will include science park development. To seize these opportunities, an "Energy Transition Strategic Group" has been established to drive strategic actions such as plant renovation, capacity enhancement, and Demo Site experiences. Additionally, "participating in government construction" and "responding to changes in customer behavior" also present development opportunities. Using the same analysis method, "Waste Management and Resource Circulation" and "Climate Strategy and Net Zero Performance" also show significant risk impacts and opportunity benefits, which will be used for further quantitative analysis.

Impact Pathway Analysis of Climate Risks and Opportunities for Material Sustainability Issues

Looking Ahead: Advancing Sustainability Solutions

The implementation of IFRS is an important foundation for deepening governance. The Task Force inventoried four enhancement directions through gap analysis, identified 8 material sustainability issues, and clarified risks and opportunities through senior executive interviews. Among these, three issues—"Net-zero EPC and Green Engineering," "Waste Management and Resource Circulation," and "Climate Strategy and Net Zero Performance"—will be prioritized for scenario setting and quantitative analysis to link with financial impacts and assess their impact on operations and finances. The quantitative results will serve as a basis for decision-making in risk management and strategic positioning, allowing for proactive response to potential risks, seizing transition opportunities, and strengthening overall competitiveness. On this basis, CTCI has incorporated sustainability concepts into daily operational management and combined IFRS to establish cross-departmental information integration processes and internal control systems, enhancing the consistency and transparency of information disclosure. Through systematic practices and standardized approaches, the company continues to drive this industry’s transformation toward a more sustainable future.